Leading financial and environmental intermediary

Connected for sustainable success

For companies, governments, and investors around the world AFS generates ideas, offers advisory services and tailored & electronic intermediary solutions. With over 175 years of experience, entrepreneurship, and collaboration, we developed a unique high-quality network with deep, embedded market knowledge. We provide our clients with investing, compliance and sustainability services and access to all relevant financial and environmental markets.

Interest

The AFS Interest Rate department dates back more than 175 years and is one of the largest independent Money and Fixed Income brokers in Europe with a global reach.

With over 45 specialists the Interest Rate department serves over 2,500 professional and eligible clients globally, from financial institutions to governments and supranational agencies

Execution and Custody Services

AFS Execution and Custody Services acts as an independent agency-only multi asset execution intermediary and custodian for the investment industry.

Energy

AFS Energy is a leading environmental solution provider. From the beginning to the end of your renewable energy strategy or carbon reduction transition we provide you with a pallet of service and a combination of advice and support in procurement, and trading opportunities.

Platform Solutions

For the sake of transparency and efficiency AFS is moving conventional brokerage and financing mediation in the primary and secondary market onto regulated OTF and MTF venues.

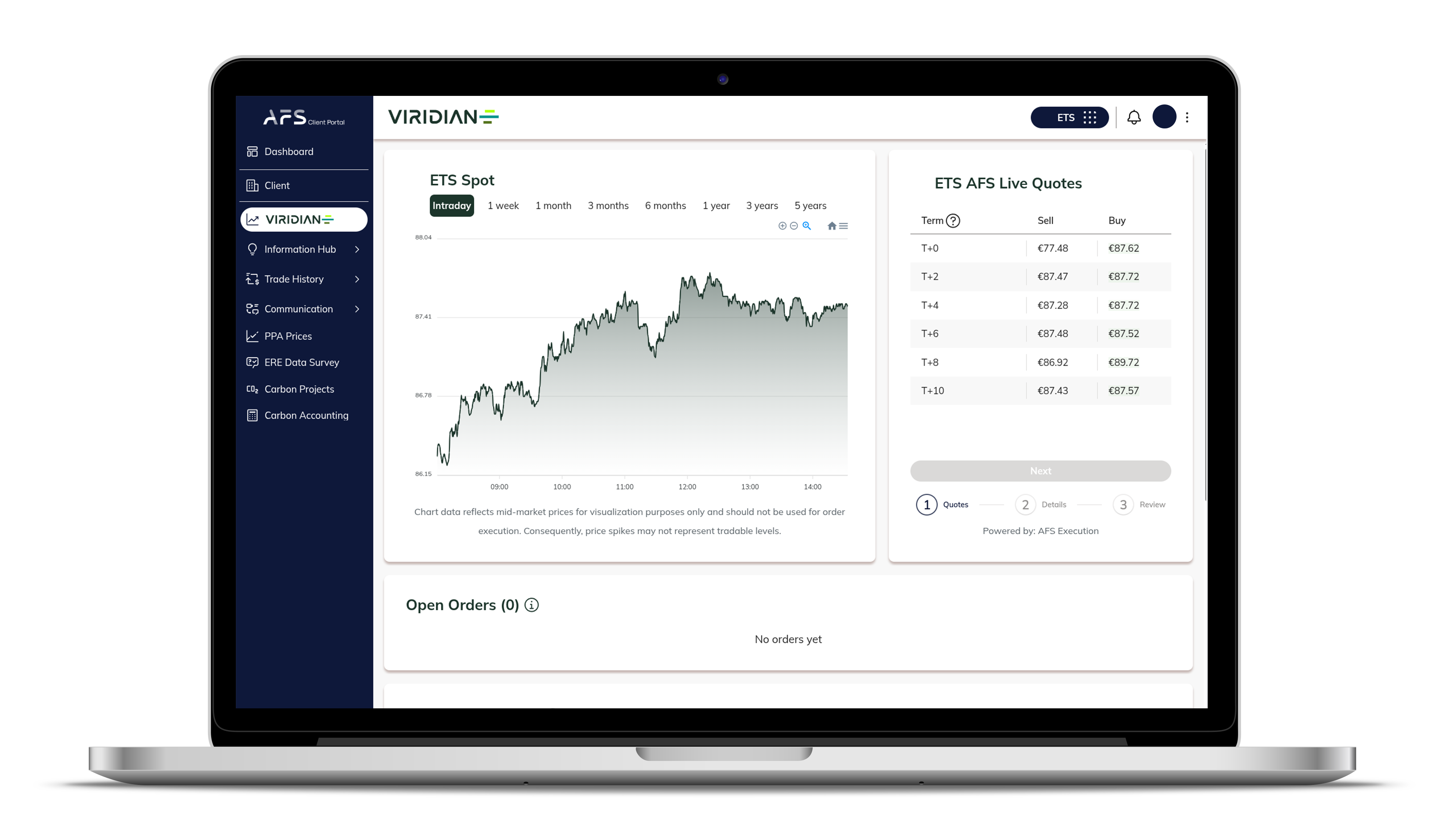

Viridian Exchange

Viridian Exchange removes the barriers to trading environmental certificates by giving you direct market access to a digital multilateral trading venue, built on clarity, certainty, and ease. Trade safely at real-time prices, execute instantly, and stay fully in control, without delays or hidden margins.

Whether you are responsible for compliance, cost control, procurement or strategic purchasing, you need to know where you stand, what you pay, and when to act. This is the offer that Viridian Exchange provides you with.

Viridian Exchange opens the EUA market for everyone

AFS has opened a new exchange called Viridian that removes the barriers to trading environmental certificates by giving you direct market access to a digital multilateral trading venue, built on clarity, certainty, and ease. Trade safely at real-time prices, execute instantly, and stay fully in control, without delays or hidden margins.

Whether you are responsible for compliance, cost control, procurement or strategic purchasing, you need to know where you stand, what you pay, and when to act. This is the offer that Viridian Exchange provides you with.From April 2026, Viridian will expand its offering to include the trading of Guarantees of Origin.

Join the fast lane

Want to know more or register? Experience what direct access feels like when transparency, security, and simplicity are the standard.

Sign up

3,000+

Active clients with more than 15 governments

180+

FTE with more than

25 nationalities

3M+

Tons CO2 offset

70+

Different instruments,

services, and products

50+

Different Countries

Latest News & Research

Stay up to date with the latest news, read our research below

.png)

AFS Group has the following accreditations:

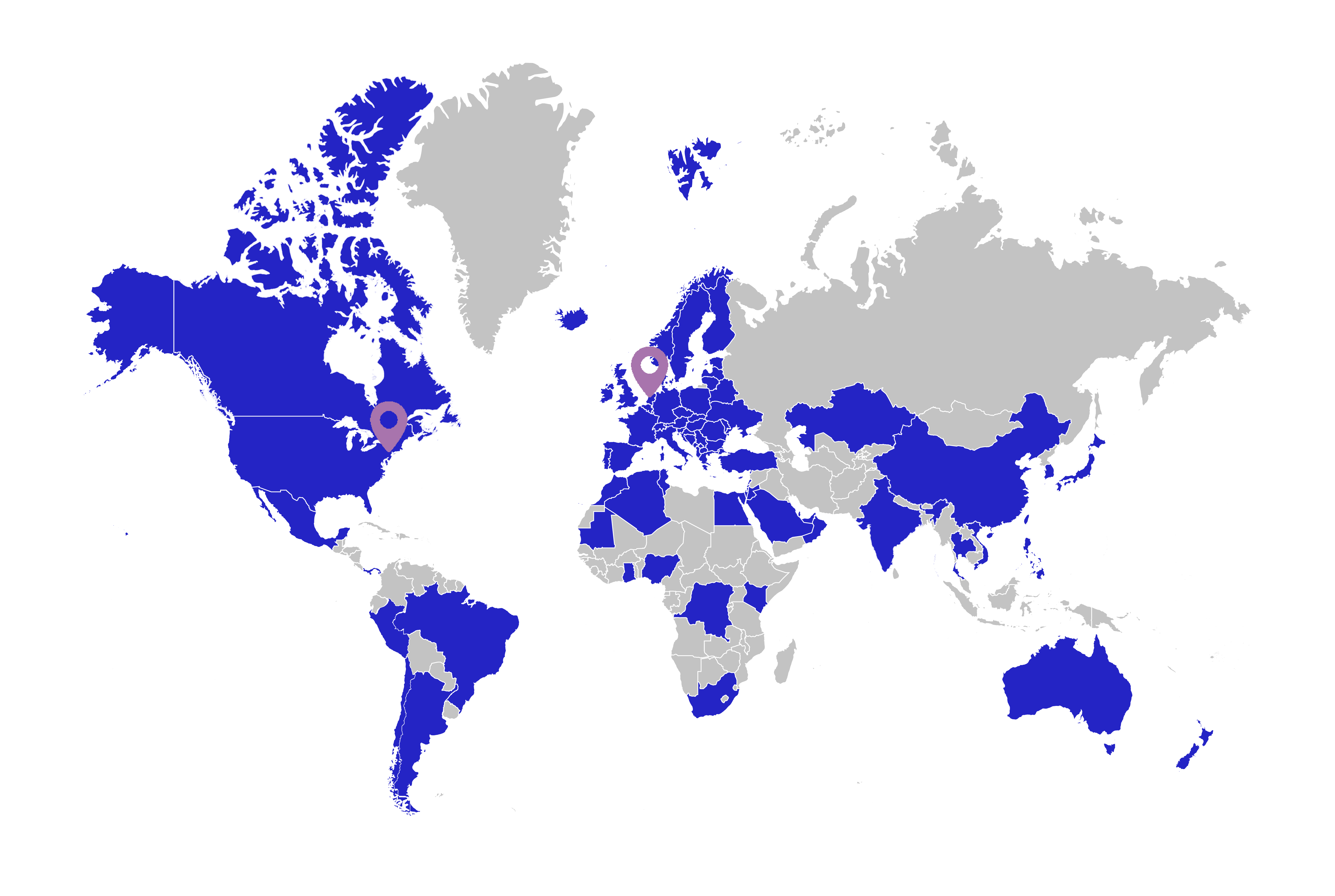

Offices & Coverage

Amsterdam

New York